🚫 The Meta-Manus Deal, a Geopolitical Flashpoint.

Plus: Top Chinese AI Models and their plus and cons.

I was quite surprised when I heard that Meta was buying Manus for $2B in December of last year, but today, that whole deal has to be reversed. This says a lot about our geopolitical situation, state power, and how nations will do anything to protect their models. We also share the top Chinese AI models list and why they are becoming the go-to open models for US companies. Let’s Dive in and Stay Curious.

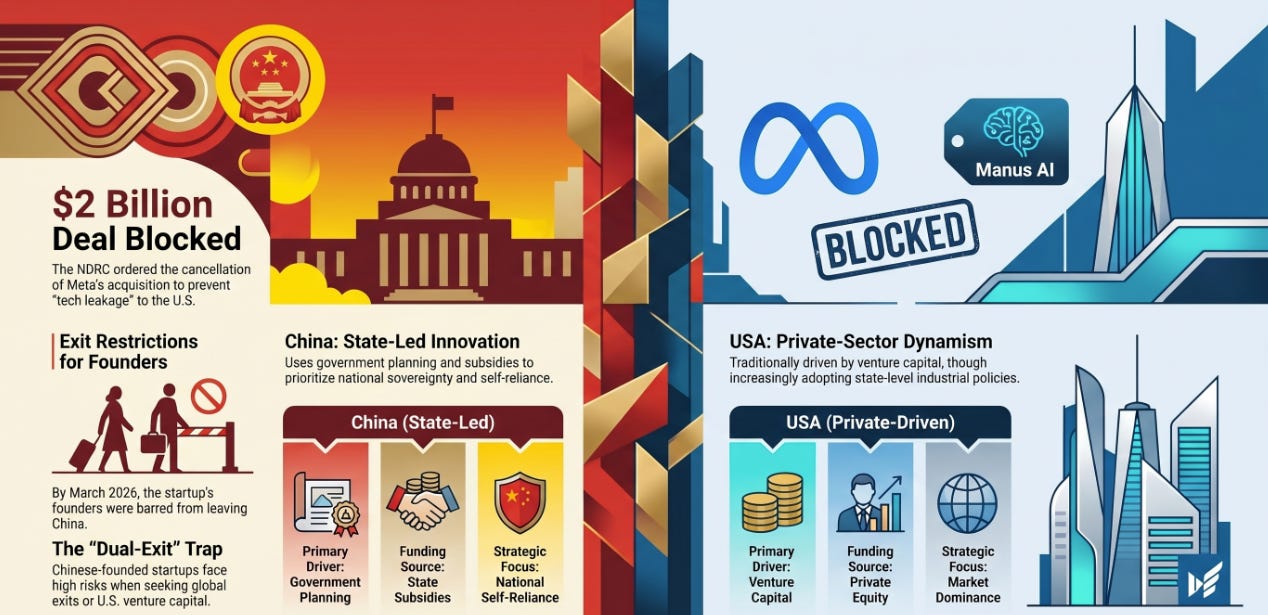

China Blocks Meta’s $2 Billion Acquisition of Manus AI

The Meta-Manus Deal: A Geopolitical Flashpoint

The New Era of Investment Restrictions

Chinese startups.

State-Driven vs. Private-Sector Models

The “Dual-Exit” Trap

🧰 AI Tools - Top Chinese AI Models

Tech Deals and Contracts at Risk in the Wake of the Meta-Manus Block

📚Learning Corner - The Elements of AI Free Courses and A 4-hour Claude Code Course. Definitely worth it.

📰 AI News and Trends

Google to invest up to $40 billion in AI rival Anthropic, days after Amazon pledged $25B. Both companies are now Anthropic’s largest investors, sole infrastructure providers, and direct competitors. Talk about circular deals.

DeepSeek previews new AI model that ‘closes the gap’ with frontier models

Meta has signed a deal to use millions of AWS Graviton chips to power its growing AI needs

OpenAI releases GPT-5.5, bringing the company one step closer to an AI ‘super app.’

Other Tech News

Samsung execs worried the company could lose money on smartphones for the first time due to high memory costs.

Tesla’s Cybercab is now in production at the company’s Gigafactory in Austin, Texas, but they are unusually cautious about the rollout.

Instagram’s new app is yet another riff on Snapchat, allowing users to post messages that disappear after a set period of time.

China Blocks Meta’s $2 Billion Acquisition of AI Startup Manus and Plans to Restrict Tech Firms From Receiving U.S. Investments.

X Money is expected to launch to the public before the end of this month. The banking and payments platform will provide free peer-to-peer transfers, a personalized metal Visa debit card, and an AI concierge that tracks spending and sorts through past transactions, getting X closer to a Super App

China Blocks Meta’s $2 Billion Acquisition of Manus AI

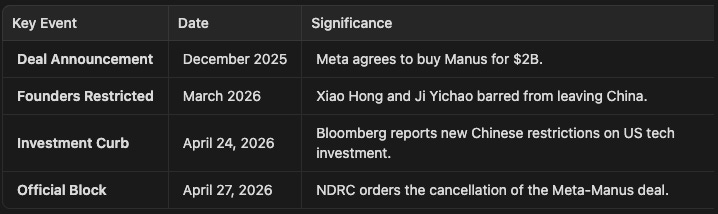

I was honestly very surprised when I heard the news that Meta was buying Manus for $2B in December of 2024. I had and have been using Manus for quite a while now, and find the model very powerful and better than some of the US rivals. SO this news seemed to me great for Meta, which I am not a fan of, and Manus investors looking to cash out, but detrimental for Manus the Model. The decision by China’s National Development and Reform Commission (NDRC) to block Meta Platforms Inc.’s $2 billion acquisition of the agentic AI startup Manus marks a watershed moment in the escalating technological rivalry between Washington and Beijing. This move, announced on April 27, 2026, represents a significant escalation in China’s efforts to prevent the “leakage” of critical artificial intelligence technology to the United States. While the deal was initially seen as a successful exit for a startup with global aspirations, it has now become a cautionary tale for the “dual-exit” risks facing Chinese-founded tech firms.

The Meta-Manus Deal: A Geopolitical Flashpoint

Manus AI, operated by Singapore-based Butterfly Effect Pte Ltd, gained global prominence for its advanced “agentic AI” autonomous systems capable of performing complex tasks independently. Founded by Chinese entrepreneurs Xiao Hong (known as Red Xiao) and Ji Yichao (Peak Ji), the startup was seen as a bridge between Chinese engineering talent and global markets. Meta’s acquisition, valued at approximately $2 billion, was intended to bolster its own AI agent capabilities.

However, the deal triggered immediate scrutiny from Beijing. Shortly after the announcement in December 2025, the NDRC launched a probe into what it termed “illegal foreign investment and tech exports.” By March 2026, the founders were reportedly barred from leaving China, and the deal was ultimately ordered to be cancelled. The NDRC’s intervention signals that Beijing now views AI talent and intellectual property as national assets that cannot be traded freely, even if the company is headquartered offshore in Singapore.

The New Era of Investment Restrictions

The blocking of the Manus deal is not an isolated incident but part of a broader strategy to curb US investment in Chinese tech companies. As reported by Bloomberg, Beijing is tightening its grip on the flow of capital and technology, driven by several factors:

Stemming Brain Drain: Beijing is increasingly concerned that its top AI researchers are being “hired away” through acquisitions by US tech giants like Meta, Google, and Microsoft.

Technology Sovereignty: The NDRC is acting as a “Chinese CFIUS” (Committee on Foreign Investment in the United States), reviewing deals not just for financial compliance but for their impact on national security and technological independence.

Reciprocal Restrictions: In response to US efforts to limit investment in Chinese AI and semiconductors, China is implementing its own “negative list” for US companies, making it nearly impossible for American firms to acquire strategic Chinese startups.

State-Driven vs. Private-Sector Models

The Manus case highlights the fundamental difference between the Chinese and American models of technological advancement. As detailed in the USCC report on Made in China 2025, China’s progress is characterized by a “comprehensive mobilization of state resources.”

The Chinese Model: State-Led Innovation

China’s approach, exemplified by the Made in China 2025 (MIC2025) initiative, relies on a multi-pronged strategy of government support. This includes massive subsidies, tax breaks, and “Government Guidance Funds” that direct capital into strategic sectors. The state also uses market entry barriers and procurement policies to favor domestic firms. This model has seen significant success in sectors like Electric Vehicles (EVs), shipbuilding, and space equipment, where China has met or exceeded its ambitious targets.

The US Model: Private-Sector Dynamism

In contrast, the US model has traditionally been driven by private enterprise, venture capital, and a highly liquid public market. Innovation is decentralized, with companies like Meta and OpenAI competing for talent and market share. However, the US is increasingly adopting an “industrial policy” of its own, such as the CHIPS Act, to counter China’s state-driven gains.

The “Dual-Exit” Trap

The blocking of the Meta-Manus deal creates a permanent “chill” in the global AI ecosystem. For founders with Chinese roots, the path to a global exit is now fraught with peril. If they sell to a US company, they risk being blocked by Beijing; if they accept US venture capital, they may face restrictions from both sides.

Moving forward, we can expect a further decoupling of the AI industry. China will likely double down on its state-driven model, providing even more capital to domestic startups to ensure they don’t feel the need to seek US buyers. Meanwhile, US companies will find it increasingly difficult to tap into the vast pool of Chinese AI talent through traditional M&A. The “Agentic AI” race, once a competition between companies, has officially become a frontline in the geopolitical struggle for technological supremacy.

📚Learning Corner

The Elements of AI - A series of free online courses created by MinnaLearn and the University of Helsinki. Learn what AI is, what can (and can’t) be done with AI, and how to start creating AI methods.

A 4-hour Claude Code Course. Definitely worth it.

Tech Deals and Contracts at Risk in the Wake of the Meta-Manus Block

The National Development and Reform Commission’s (NDRC) decision to block Meta’s acquisition of Manus AI has sent shockwaves through the global technology sector. This intervention is not merely a single-case rejection but a signal of a new, more aggressive phase in China’s “technology sovereignty” strategy. The following analysis outlines the specific deals, partnerships, and contracts that are now at high risk.

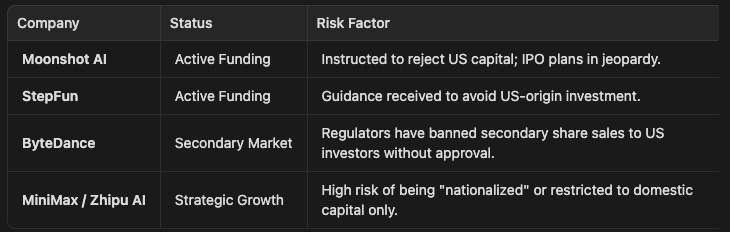

1. High-Profile AI Startups: The Funding Freeze

Beijing has moved to insulate its “national champions” in the AI sector from American influence. Regulators have reportedly issued direct guidance to several top-tier AI startups to reject US capital in future funding rounds.

For these companies, the “dual-exit” trap is now a reality. They are effectively barred from being acquired by US tech giants (the Meta-Manus precedent) and are increasingly restricted from accessing the world’s deepest pool of venture capital.

2. Strategic Partnerships and Global Alliances

The “chilling effect” extends beyond direct acquisitions to complex global partnerships that involve US technology and Chinese-linked entities.

•Microsoft and G42: Microsoft’s $1.5 billion investment in the UAE-based AI firm G42 is under intense scrutiny. Because G42 has historical ties to Chinese hardware and talent, US regulators fear it could serve as a “backdoor” for tech leakage. Conversely, China may now view G42’s pivot toward Microsoft as a betrayal of technological cooperation, potentially leading to the cancellation of G42’s existing contracts within China.

•OpenAI’s Global Expansion: As OpenAI seeks to expand its footprint in Asia and the Middle East, any partnership involving entities with significant Chinese ties will be a non-starter. The Meta-Manus block confirms that even “neutral” hubs like Singapore or the UAE are no longer safe harbors for US-China tech collaboration.

3. Supply Chain and Operational Contracts

The most significant financial impact may be felt in the multi-billion-dollar supply chain contracts that underpin the global hardware industry.

The Nvidia “H20” Crisis

NVIDIA developed the H20 chip specifically to comply with US export controls while still serving the Chinese market. However, Beijing has reportedly retaliated by directing Chinese firms to stop purchasing Nvidia hardware altogether in favor of domestic alternatives like the Huawei Ascend series. Reports of Nvidia halting H20 production suggest that this multi-billion dollar revenue stream is effectively at an end.

Apple’s “China-Light” Strategy

Apple is accelerating its shift of iPhone production to India and Vietnam, aiming for India to produce the majority of US-bound iPhones by the end of 2026. This transition puts long-term contracts with Chinese manufacturing giants like Luxshare and Foxconn’s mainland facilities at risk. As Apple moves its “center of gravity” away from China, Beijing may respond by making it harder for Apple to operate its retail and services business within the country.

Tesla’s Data Security Tightrope

Tesla’s rollout of Full Self-Driving (FSD) in China is contingent on complex data security contracts and government approvals. In the current climate, Beijing may demand full “data sovereignty,” requiring Tesla to store and process all AI training data locally and potentially barring the export of any “learned” weights back to the US. This would effectively split Tesla’s AI development into two incompatible silos.

4. The Future of Venture Capital

The era of the “global venture fund” is effectively over. The split of Sequoia Capital into separate US and China (HongShan) entities was the first major tremor; the Meta-Manus block is the earthquake. US pension funds and endowments, which have historically been the primary backers of Chinese tech growth, are now facing immense pressure to divest. This capital flight will force Chinese startups to rely entirely on state-backed “Guidance Funds,” further cementing the state-driven development model.

Conclusion: The Decoupling of the AI Ecosystem

The Meta-Manus block has proven that technology is no longer a private commodity but a national security asset. Any contract or deal that involves the transfer of “agentic” or “frontier” AI capabilities across the US-China divide is now considered high-risk. We are witnessing the birth of two distinct, non-interoperable technological ecosystems, where the price of entry is total alignment with one side or the other.

🧰 AI Tools of The Day

Top Chinese AI Models

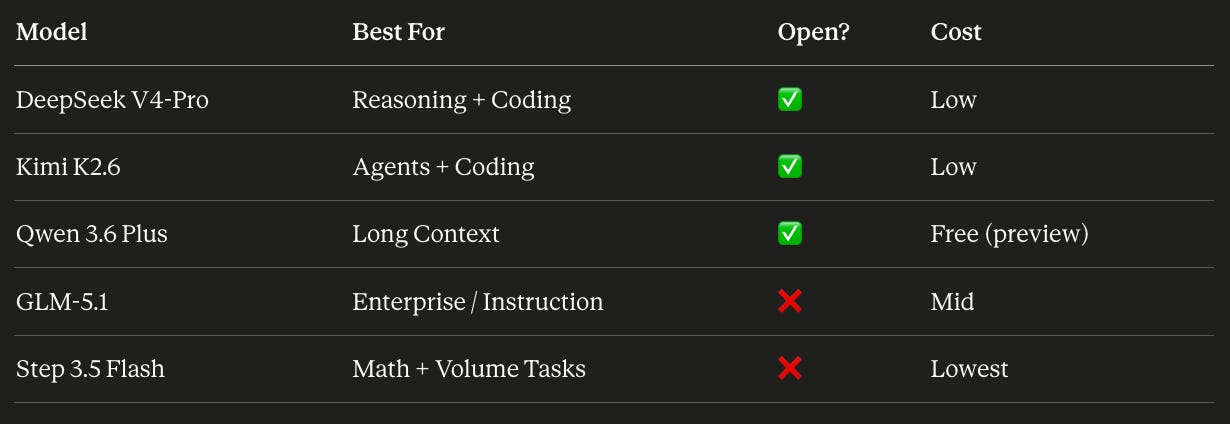

🥇 1. DeepSeek V4-Pro - Trailing only Google’s Gemini 3.1-Pro on world knowledge, and falling only marginally short of GPT-5.4 overall. Like its predecessors, V4-Pro is fully open-source, which has been China’s key competitive strategy, rapidly scaling adoption while working around US chip export restrictions.

🥈 2. Kimi K2.6 - Scores 80.2% on SWE-Bench Verified, supports agentic workflows, and became the first open-weight model to beat GPT-5.4 on the SWE-Bench Pro coding benchmark. For coding and agent workloads, it’s the top Chinese pick, and costs roughly 75% less than GPT-5.4 at comparable quality.

🥉 3. Qwen 3.6 Plus — Go-to for long-context tasks, offering 1 million token context windows, and is currently free during its preview period. Alibaba’s Qwen family now has the most user-generated variants on Hugging Face, more than Google and Meta combined.

4️⃣ GLM-5.1 (Z.AI / Zhipu AI) - #3 on benchmark leaderboards with a score of 83, with strong math (89) and instruction following (93). GLM-5 Reasoning leads Chinese models in agentic capability, with scores of 88 in reasoning and 86 in agentic tasks. GLM-5.1 beat Claude Opus 4.6 on a key coding benchmark earlier this quarter.

5 - Step 3.5 Flash - ships at $0.10/$0.30 per million tokens, 25× cheaper than GPT-4o with comparable math reasoning. For agent workloads with stable system prompts, effective input cost can drop to as low as $0.03–0.07 per million tokens.

📊 Quick Comparison

Bottom line: Chinese AI labs are shipping frontier coding models faster than most developers can keep up — and at least three Chinese models now score above 75% on SWE-Bench Verified, putting them in direct competition with GPT-5.4 and Claude 4.5 Sonnet. The price gap alone makes these worth integrating into your client service stack.